Understanding the 2025 tax brackets for married filing jointly is essential for accurate tax planning, withholding adjustments, and year‑end financial strategy. Each year, the IRS adjusts more than 60 tax provisions including income tax brackets to prevent “bracket creep,” where inflation pushes taxpayers into higher tax rates even if their purchasing power hasn’t increased. For 2025, the IRS applied a roughly 2.8% inflation adjustment to federal tax parameters.

This guide breaks down the 2025 federal income tax brackets, the standard deduction, and what married couples should consider when planning for the year.

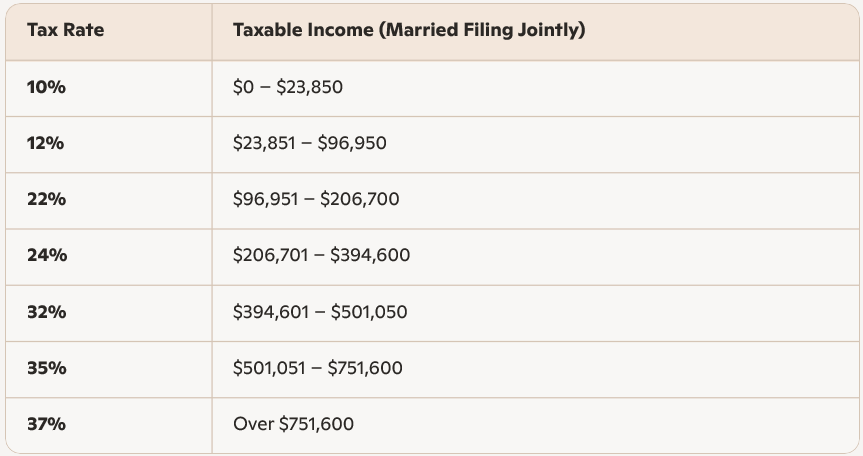

What Are the 2025 Tax Brackets for Married Filing Jointly?

The IRS maintains seven marginal tax rates: 10%, 12%, 22%, 24%, 32%, 35%, and 37%. These rates apply to different layers of income, not your entire taxable income. For 2025, the income thresholds for each bracket increased to reflect inflation.

2025 Federal Income Tax Brackets (Married Filing Jointly)

According to the Tax Foundation’s IRS‑based analysis, the 2025 brackets for married couples filing jointly are as follows:

The top marginal rate of 37% applies only to income above $751,600 for married joint filers.

2025 Standard Deduction for Married Filing Jointly

The standard deduction also increases annually to keep pace with inflation. For 2025, the IRS set the standard deduction at:

- $30,000 for married couples filing jointly

This deduction reduces taxable income before tax brackets are applied, lowering the overall tax burden.

Additional Standard Deduction

For taxpayers 65 or older or blind, the additional deduction is:

- $1,600 per qualifying spouse (married filing jointly)

How the 2025 Brackets Compare to 2024 For Married Filers

While the IRS has not yet published the full 2025 tables on its website, independent analyses confirm that all bracket thresholds increased by roughly 2.8% due to inflation adjustments under the Chained CPI formula.

This means:

- More of your income is taxed at lower rates.

- You may owe less tax even if your income stayed the same.

- Withholding adjustments may be necessary to avoid over‑ or under‑paying.

Why the 2025 Tax Brackets Matter for Married Couples

1. Better Tax Planning

Knowing your bracket helps you plan:

- Roth vs. traditional IRA contributions

- Timing of bonuses or capital gains

- Charitable giving strategies

2. Withholding Adjustments

If your income changed in 2024 or will change in 2025, updating your W‑4 can prevent surprises at tax time.

3. Retirement Contribution Optimization

Higher brackets may encourage:

- Maxing out 401(k) or 403(b) contributions

- Using pre‑tax accounts to reduce taxable income

4. Strategic Income Timing

Married couples with variable income—such as business owners or commission earners—can time income or deductions to stay within a lower bracket.

Example: How a Married Couple’s Taxes Are Calculated in 2025

Suppose a married couple has $180,000 in taxable income after deductions.

Their tax would be calculated in layers:

- 10% on the first $23,850

- 12% on income from $23,851 to $96,950

- 22% on income from $96,951 to $180,000

This progressive structure ensures they do not pay 22% on their entire income—only on the portion within that bracket.

Key IRS Rules Affecting 2025 Brackets

Inflation Adjustments

The IRS uses the Chained Consumer Price Index (C‑CPI) to adjust tax parameters annually, a change implemented by the 2017 Tax Cuts and Jobs Act.

Tips for Married Couples Filing Jointly in 2025

Review Your Withholding Early

Use the IRS withholding estimator to avoid underpayment penalties.

Maximize Tax‑Advantaged Accounts

- 401(k)

- HSA

- Traditional IRA

These reduce taxable income and may keep you in a lower bracket.

Consider Bunching Deductions

If you itemize, grouping charitable donations or medical expenses into one year can increase tax savings.

Plan Capital Gains Carefully

Long‑term capital gains have their own brackets, which interact with ordinary income thresholds.

Final Thoughts

The 2025 tax brackets for married filing jointly offer slightly higher income thresholds across all rates, giving couples more room before hitting higher tax levels. With the standard deduction rising to $30,000, many households will see a modest reduction in taxable income.

Understanding these brackets helps married couples make smarter financial decisions, optimize retirement contributions, and avoid tax‑time surprises.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.