Planning ahead for retirement is all about timing, and when it comes to Individual Retirement Accounts (IRAs), deadlines matter just as much as contribution limits. Missing the cutoff can mean losing valuable tax advantages and compounding growth opportunities. This article breaks down the 2026 IRA contribution deadlines, limits, and strategies to maximize your retirement savings.

Key IRA Contribution Deadlines in 2026

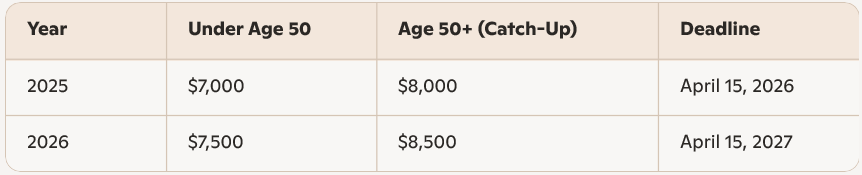

- 2025 Tax Year Contributions: You have until April 15, 2026 (Tax Day) to contribute to your IRA for the 2025 tax year.

- 2026 Tax Year Contributions: Starting January 1, 2026, you can contribute toward your 2026 IRA limit. The deadline for these contributions is April 15, 2027.

- No Extensions: Filing a tax extension does not extend your IRA contribution deadline.

IRA Contribution Limits and Deadlines for 2026

The IRS sets annual limits that determine how much you can contribute:

Traditional vs. Roth IRA Rules

- Traditional IRA: Contributions are made with pre-tax dollars. You’ll pay taxes when you withdraw funds in retirement.

- Roth IRA: Contributions are made with after-tax dollars. Qualified withdrawals in retirement are tax-free.

- Eligibility: Roth IRA contributions depend on your Modified Adjusted Gross Income (MAGI). Exceeding income thresholds may require a backdoor Roth strategy.

Common Mistakes to Avoid

- Missing the Deadline: Waiting until the last minute risks errors or missed contributions.

- Incorrect Year Designation: Between January 1 and April 15, you must specify whether your contribution is for the prior year or current year. A wrong designation can trigger penalties.

- Excess Contributions: Contributing beyond the limit results in a 6% annual penalty until corrected.

- Ignoring Income Limits: High earners may be ineligible for direct Roth contributions.

Why Contributing Early Matters

Contributing early in the year maximizes the power of compounding. For example:

- A $7,500 contribution made in January 2026 has 15 extra months to grow compared to one made at the April 2027 deadline.

- Over decades, this timing difference can add thousands of dollars to your retirement balance.

Action Plan for 2026 IRA Contribution Deadlines

- Mark Your Calendar: April 15, 2026 for 2025 contributions; April 15, 2027 for 2026 contributions.

- Automate Contributions: Set up monthly transfers to avoid last-minute stress.

- Check Eligibility: Review income thresholds for Roth IRAs.

- Maximize Limits: Take advantage of catch-up contributions if you’re 50 or older.

- Consult a Professional: A financial advisor can help tailor strategies to your income and retirement goals.

Risks and Trade-Offs

- Penalty Risk: Excess contributions cost 6% annually until fixed.

- Lost Growth: Delayed contributions mean less compounding.

- Income Restrictions: High earners may need alternative strategies like backdoor Roth conversions.

Conclusion

The 2026 IRA contribution deadlines are straightforward but critical: April 15, 2026 for 2025 contributions and April 15, 2027 for 2026 contributions. With limits set at $7,500 (under 50) and $8,500 (50+), planning ahead ensures you maximize tax advantages and retirement growth. By contributing early, avoiding common mistakes, and staying mindful of eligibility rules, you can make the most of your IRA in 2026 and beyond.