Introduction

If you’ve ever wondered how to do a back door Roth, you’re not alone. High-income earners often face IRS limits that prevent direct Roth IRA contributions. Fortunately, the back door Roth strategy provides a legal workaround, allowing you to enjoy tax-free growth and withdrawals in retirement. This article explains how to do a back door Roth contribution step by step, highlights IRS rules, and shows why this strategy is so powerful.

What Is a Back Door Roth IRA?

A back door Roth IRA isn’t a special account—it’s a method. Learning how to do this means understanding two simple steps:

- Contribute to a traditional IRA (usually nondeductible).

- Convert that contribution into a Roth IRA.

Because Roth conversions have no income limits, this strategy bypasses restrictions and unlocks Roth benefits.

Why Learn How to Do a Back Door Roth?

- Tax-Free Growth: Once converted, your investments grow tax-free.

- Tax-Free Withdrawals: Qualified distributions in retirement are not taxed.

- No RMDs: Roth IRAs don’t require withdrawals at age 73.

- Estate Planning Benefits: Assets can pass to heirs tax-free.

For high earners, knowing how to do this can be a game-changer in retirement planning.

Step-by-Step Guide: How to Do a Back Door Roth Contribution

Step 1: Confirm Eligibility

- For 2024, Roth IRA contributions phase out at $146,000–$161,000 MAGI for single filers and $230,000–$240,000 for married couples filing jointly.

- If your income exceeds these limits, you’ll need to learn how to do a back door Roth.

Step 2: Open a Traditional IRA

- If you don’t already have one, open a traditional IRA with a brokerage firm.

- Contribution limits for 2024: $7,000 per year (or $8,000 if age 50+).

Step 3: Make a Nondeductible Contribution

- Contribute after-tax dollars to your traditional IRA.

- File IRS Form 8606 to report nondeductible contributions.

Step 4: Convert to a Roth IRA

- Transfer the funds from your traditional IRA into a Roth IRA.

- Convert soon after contributing to minimize taxable gains.

Step 5: Handle Taxes Properly

- If you only contributed nondeductible dollars, the conversion is generally tax-free.

- If you have other pre-tax IRA balances, the pro-rata rule applies, meaning part of your conversion may be taxable.

Key Rules When Learning How to Do a Back Door Roth

The Pro-Rata Rule

If you hold pre-tax IRA funds, the IRS requires you to calculate the taxable portion of your conversion proportionally. This is one of the most important rules to understand when learning how to do a back door Roth correctly.

The Five-Year Rule

Converted funds must remain in the Roth for five years before penalty-free withdrawals, even if you’re over 59½.

Catch-Up Contributions

If you’re 50 or older, you can contribute an extra $1,000 annually.

Timing Matters

Convert quickly after contributing to avoid taxable investment gains.

Common Mistakes to Avoid

- Skipping IRS Form 8606: Without it, you risk double taxation.

- Ignoring the Pro-Rata Rule: Not accounting for existing pre-tax IRA balances can lead to unexpected taxes.

- Delaying Conversion: Waiting too long allows earnings to accumulate, which become taxable upon conversion.

Avoiding these mistakes is essential if you want to master how to do a back door Roth contribution.

FAQs On How to Do a Back Door Roth Contribution

Can anyone learn how to do this?

Yes, as long as you have earned income and your contribution doesn’t exceed annual limits.

Is a back door Roth IRA legal?

Absolutely. The IRS recognizes Roth conversions regardless of income level.

Do I owe taxes when I do this?

If you only contributed nondeductible dollars, usually no. But pre-tax balances trigger taxes under the pro-rata rule.

What forms do I need?

You’ll need IRS Form 8606 to report nondeductible contributions and conversions.

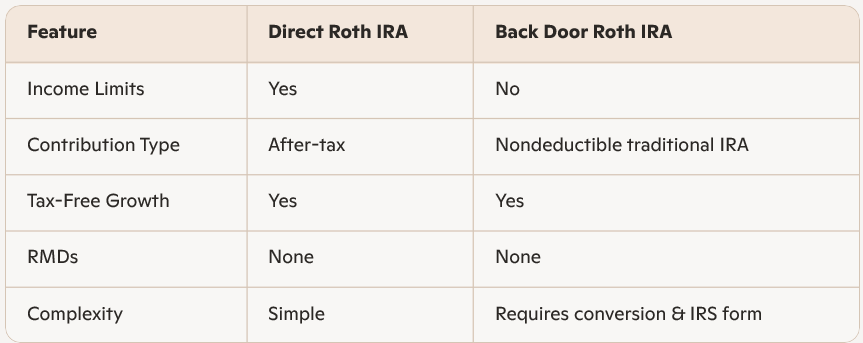

Comparison: Direct Roth vs. Back Door Roth

Conclusion

Understanding how to do a back door Roth contribution is essential for high-income earners who want tax-free retirement savings. By contributing to a traditional IRA and converting to a Roth, you unlock powerful benefits like tax-free growth, no RMDs, and estate planning advantages. The process requires careful attention to IRS rules—especially the pro-rata rule and proper filing of Form 8606—but when done correctly, it can significantly enhance your retirement strategy