If you’re going to be receiving Social Security benefits in 2026 and considering working—whether part-time or full-time—it’s essential to understand how your earnings may impact your monthly payments. Working while collecting Social Security can reduce your benefits temporarily if you’re under full retirement age (FRA), but it can also increase your lifetime payout. Here’s a comprehensive guide to help you navigate the rules, limits, and strategies in 2026 and the rest of 2025.

Can You Work While Receiving Social Security Benefits In 2026?

Yes, you can work while receiving Social Security retirement benefits. However, if you haven’t reached your Full Retirement Age (FRA)—which is 67 for those born in 1960 or later—your benefits may be temporarily reduced based on how much you earn.

The Social Security Administration (SSA) uses an earnings test to determine whether your income exceeds annual limits. If it does, a portion of your benefits will be withheld. But here’s the good news: these reductions are not permanent. Once you reach FRA, your benefits are recalculated to account for the withheld amounts, often resulting in higher monthly payments.

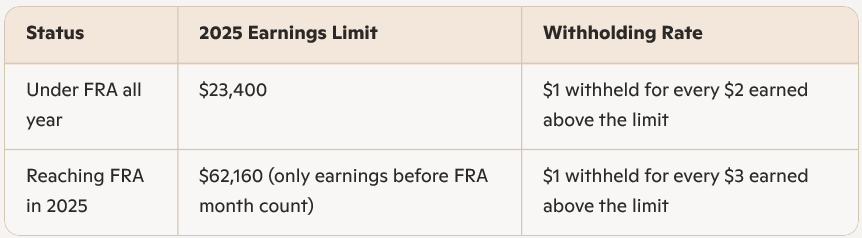

2025 Earnings Limits and Withholding Rules

The SSA sets two different earnings limits depending on your age:

Example: If you’re 64 and earn $30,000 in 2025, you’re $6,600 over the limit. SSA will withhold $3,300 from your benefits that year.

What Happens to Withheld Social Security Benefits In 2026?

Many retirees worry that withheld benefits are lost forever. That’s a myth. Once you reach FRA, the SSA recalculates your benefit to credit back the months when payments were reduced. This means your future monthly checks will be higher, helping you recover the withheld amount over time.

Strategic Considerations Before You Work

Working in retirement can be financially and emotionally rewarding. But before you take a job while receiving Social Security, consider these factors:

- Impact on immediate cash flow: If your earnings exceed the limit, your monthly benefits may be reduced, which could affect your budget.

- Long-term benefit increase: Continued work can replace lower-earning years in your 35-year earnings history, potentially boosting your benefit calculation.

- Delaying benefits: If you haven’t claimed yet, delaying Social Security past FRA increases your benefit by about 8% per year until age 70.

What Counts as Earnings?

Only wages from employment or net self-employment income count toward the earnings test. This includes:

- Salaries

- Bonuses

- Commissions

- Vacation pay

Excluded income:

- Pensions

- Annuities

- Investment income

- Veterans benefits

- Government or military retirement benefits

Annual Recalculation and COLA Adjustments

Each year, the SSA reviews your earnings to determine if your benefit should be increased. If your recent income replaces a lower year in your earnings record, your monthly benefit may rise. Additionally, Cost-of-Living Adjustments (COLA) are applied annually. In 2026, for example, retirees will receive a 2.8% COLA increase, adding about $56 per month to the average benefit.

Planning Tips for Working Retirees

To maximize your Social Security benefits while working:

- Track your earnings: Stay below the annual limit if you want to avoid reductions.

- Use SSA calculators: Estimate how your income will affect benefits.

- Report changes promptly: Notify SSA if your earnings differ from your initial estimate.

- Coordinate with your spouse: Joint planning can optimize household income.

- Consult a financial advisor: Professional guidance can help tailor your strategy.

Looking Ahead: Changes To Social Security Benefits in 2026

The SSA has announced higher earnings limits for 2026, which means you’ll be able to earn more before facing benefit reductions:

- Under FRA: Limit increases to $24,480

- Reaching FRA in 2026: Limit increases to $65,160

These changes will allow retirees to keep more of their benefits while working.

Final Thoughts

Working while receiving Social Security benefits in 2026 is entirely possible—but it requires careful planning. Understand the earnings limits, track your income, and consider the long-term impact on your benefits. Whether you’re working for financial necessity or personal fulfillment, staying informed ensures you make the most of your retirement years.