Understanding how capital gain distributions are taxed is essential for anyone who invests in mutual funds or exchange‑traded funds (ETFs). These distributions can catch investors off guard—especially when they owe taxes on gains even if they never sold a single share. Whether you’re building a long‑term portfolio or fine‑tuning your tax strategy, knowing the rules can help you avoid surprises and keep more of your investment returns.

This guide breaks down what capital gain distributions are, why they happen, and how capital gain distributions are taxed under current IRS rules.

What Are Capital Gain Distributions?

Capital gain distributions occur when a mutual fund or ETF sells securities inside the fund for a profit. These gains are then passed on to shareholders, typically once per year. You might receive two types of gains:

- Short‑term capital gain distributions

- Long‑term capital gain distributions

Even if you reinvest these distributions back into the fund, the IRS still treats them as taxable income in the year they’re paid.

Why Do Funds Make Capital Gain Distributions?

Funds buy and sell securities throughout the year. When they sell holdings that have appreciated, the fund realizes a capital gain. By law, most funds must distribute these gains to shareholders to avoid paying corporate‑level taxes.

Common reasons funds generate gains include:

- Portfolio rebalancing

- Manager strategy changes

- Investor redemptions forcing the fund to sell assets

- Market volatility creating opportunities to lock in profits

This is why investors sometimes receive large capital gain distributions even in years when the fund’s share price declines.

How Capital Gain Distributions Are Taxed

The IRS taxes capital gain distributions based on the type of gain the fund realized not how long you held your shares. This is one of the most important distinctions for investors.

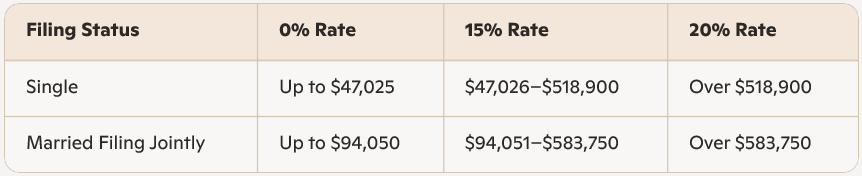

1. Long‑Term Capital Gain Distributions

Most capital gain distributions are long‑term. These are taxed at the favorable long‑term capital gains rates:

(Thresholds shown for illustration; actual brackets may vary by tax year.)

Long‑term distributions are reported on Form 1099‑DIV, Box 2a.

2. Short‑Term Capital Gain Distributions

Short‑term gains occur when the fund sells investments held for one year or less. These are taxed as ordinary income, using your regular tax bracket.

They appear on Form 1099‑DIV, Box 1a, lumped in with ordinary dividends.

3. State Taxes

Most states tax capital gain distributions as ordinary income, though a few offer preferential treatment for long‑term gains. Always check your state’s rules.

How Reinvested Capital Gain Distributions Are Taxed

Many investors reinvest distributions automatically. While this boosts your cost basis (reducing future taxable gains), it does not eliminate the tax owed in the year of the distribution.

In other words:

- Reinvesting = still taxable

- Reinvested amount increases your basis

- Higher basis reduces future capital gains when you sell

This is a key concept in understanding these distributions.

Capital Gain Distributions in Tax‑Advantaged Accounts

The tax treatment changes dramatically depending on the type of account.

1. Traditional IRA, Roth IRA, 401(k), and Similar Accounts

Inside tax‑advantaged accounts:

- Capital gain distributions are not taxed when paid

- You do not report them on your tax return

- Taxes apply only when you withdraw (Traditional) or not at all (qualified Roth withdrawals)

This is why many investors prefer holding actively managed funds inside retirement accounts.

2. Taxable Brokerage Accounts

In taxable accounts, all capital gain distributions are taxable in the year received, regardless of reinvestment.

How to Reduce or Avoid Capital Gain Distribution Taxes

Smart investors use several strategies to minimize taxes:

1. Favor Tax‑Efficient Funds

Index funds and ETFs typically generate fewer taxable gains because they trade less frequently.

2. Use Tax‑Advantaged Accounts

Hold actively managed funds in IRAs or 401(k)s to avoid annual taxation.

3. Harvest Losses

Tax‑loss harvesting can offset capital gain distributions.

4. Check Distribution Estimates Before Buying

Buying a fund right before a large distribution can trigger an immediate tax bill. Many fund companies publish estimates in November or December.

5. Consider Municipal Bond Funds

These often generate little or no taxable capital gains.

Reporting Capital Gain Distributions on Your Tax Return

You’ll receive Form 1099‑DIV from your brokerage each year. Key boxes include:

- Box 1a: Ordinary dividends (includes short‑term capital gain distributions)

- Box 1b: Qualified dividends

- Box 2a: Total long‑term capital gain distributions

You report these amounts on Schedule D and Form 1040, unless you qualify for simplified reporting.

Final Thoughts

However, understanding how capital gain distributions are taxed helps you make smarter investment decisions and avoid unexpected tax bills. While these distributions are a normal part of owning mutual funds and ETFs, strategic planning such as using tax‑advantaged accounts, choosing tax‑efficient funds, and timing purchases can significantly reduce your tax burden.

If you’re building a tax‑smart portfolio, knowing the rules around capital gain distributions is one of the most effective ways to protect your returns and optimize long‑term wealth.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.