Bonus depreciation has undergone one of its most significant transformations in decades and 2026 is the first full year where businesses can take advantage of the new permanent 100% first‑year deduction created by the One Big Beautiful Bill Act (OBBBA). Whether you’re a small business owner, real estate investor, or CFO planning capital expenditures, understanding these rules is essential for maximizing tax savings.

In January 2026, the IRS released Notice 2026‑11, providing interim guidance on how taxpayers should apply the updated rules. The headline: 100% bonus depreciation is now permanent for qualified property acquired after January 19, 2025.

This article breaks down everything you need to know for 2026 eligibility, planning strategies, elections, and how the new rules differ from the TCJA framework.

1. Bonus Depreciation Is Now Permanently Set at 100%

Under the OBBBA, bonus depreciation no longer phases down. Instead, qualified property acquired and placed in service after January 19, 2025, receives a full 100% first‑year deduction.

This is a major shift from the Tax Cuts and Jobs Act (TCJA), which had scheduled bonus depreciation to drop to 20% by 2026. The new law eliminates that decline entirely.

What qualifies?

Property must meet the following criteria:

- Acquired after January 19, 2025

- Original use begins with the taxpayer (or meets used‑property rules)

- MACRS recovery period of 20 years or less

- Certain computer software

- Water utility property

- Qualified film, TV, theatrical productions

- Newly added: qualified sound recording productions

The OBBBA also expands eligibility to certain manufacturing‑related assets, pending future regulations.

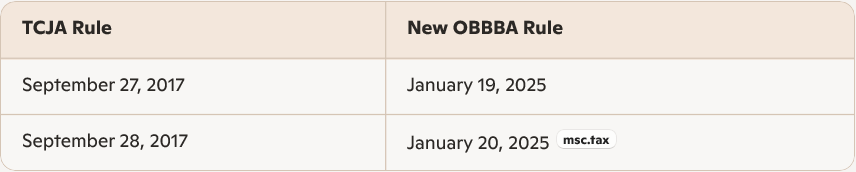

2. The TCJA Framework Still Applies But With New Dates

Notice 2026‑11 confirms that the IRS will continue using the familiar TCJA rules to determine when property is “acquired.” The only change is the cutoff dates:

This means the same tests still apply:

- Written Binding Contract (WBC) Test

- Physical Work of a Significant Nature Test

- 10% Safe Harbor

- Preliminary Activity Exclusion

If a project began under a binding contract before January 20, 2025, it may fall under the old TCJA phase‑down rules instead of the new permanent 100%.

3. No More Placed‑in‑Service Deadlines

One of the most taxpayer‑friendly changes is the elimination of placed‑in‑service deadlines.

Under the TCJA, property generally had to be placed in service by 2027 (or 2028 for long‑production‑period property and aircraft). The OBBBA removes these deadlines entirely.

What this means for 2026 planning

- Multi‑year construction projects no longer risk missing a placed‑in‑service cutoff.

- Businesses can plan capital expenditures without timing pressure.

- Cost segregation studies become even more valuable because all qualifying components can receive 100% bonus depreciation regardless of service date.

4. New Elections Available Under Notice 2026‑11

The IRS guidance outlines several elections taxpayers may make for 2026 and beyond. These include:

Electing 40% (or 60%) Instead of 100%

Taxpayers may elect:

- 40% bonus depreciation, or

- 60% for certain long‑production‑period property or aircraft

This may be beneficial when:

- You want to smooth taxable income over multiple years

- You expect higher future tax rates

- You want to avoid creating or increasing NOLs

Electing Out of Bonus Depreciation

Taxpayers may elect not to claim bonus depreciation for:

- A class of property

- Qualified sound recording productions

Specified Plant Elections

Businesses may elect bonus depreciation for:

- Trees

- Vines

- Fruit‑bearing plants, when planted or grafted after January 19, 2025.

Component Election for Self‑Constructed Property

Taxpayers may elect to treat certain components of larger self‑constructed property as eligible for bonus depreciation an important planning tool for large construction projects.

5. Expanded Eligible Property Categories

The OBBBA adds new categories of property eligible for bonus depreciation, including:

- Qualified sound recording productions

- Qualified production property under §168(n)

- Certain manufacturing‑related assets

This expansion is particularly beneficial for:

- Music producers and studios

- Film and media companies

- Manufacturing facilities investing in new equipment

6. Planning Strategies for 2026 Bonus Depreciation

A. Accelerate Acquisitions After January 19, 2025

To qualify for the permanent 100% deduction, ensure assets are acquired after the cutoff date not just delivered.

B. Use Cost Segregation to Maximize Deductions

Cost segregation can reclassify building components into 5‑, 7‑, or 15‑year property, all of which qualify for 100% bonus depreciation.

C. Consider Electing Lower Bonus Rates

If your business expects:

- Higher future tax rates

- Large upcoming income

- Or wants to avoid NOL selecting 40% or 60% may be strategic.

D. Review Contracts for Binding Contract Rules

A contract signed before January 20, 2025 may disqualify property from the new rules even if placed in service in 2026.

7. Who Benefits Most in 2026?

- Construction companies with multi‑year projects

- Manufacturers investing in equipment

- Real estate investors using cost segregation

- Media and entertainment companies (especially with new sound recording eligibility)

- Small businesses purchasing machinery, vehicles, and technology

Final Thoughts About Bonus Depreciation in 2026

The 2026 tax year marks a new era for bonus depreciation. With permanent 100% expensing, expanded eligible property categories, and the removal of placed‑in‑service deadlines, businesses have more flexibility and more opportunities to reduce taxable income than ever before.

Understanding the acquisition rules, elections, and planning strategies is essential for maximizing the benefit. As IRS regulations continue to evolve, staying informed will ensure you capture every available deduction.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.