Non‑recourse debt is a powerful financial tool that plays a major role in real estate investing, business financing, and asset‑backed lending. While it may sound technical, understanding how non‑recourse loans work can help investors reduce personal risk, protect assets, and make smarter long‑term financial decisions. This guide breaks down the essentials of non‑recourse debt, how it compares to recourse loans, and when it may be the right choice.

What Is Non‑Recourse Debt?

Non‑recourse debt is a type of loan in which the lender’s only remedy in the event of default is to seize the collateral securing the loan. The borrower is not personally liable beyond the pledged asset. If the collateral doesn’t fully cover the outstanding balance, the lender cannot pursue the borrower’s personal assets, wages, or future income.

In simple terms:

If you default, the lender can take the asset—but nothing more.

This structure makes non‑recourse loans especially attractive for investors who want to limit downside risk.

How Non‑Recourse Debt Works

Non‑recourse loans are typically secured by a specific asset, such as:

- Real estate (commercial or investment property)

- Equipment

- Vehicles

- Investment portfolios

- Business assets

If the borrower fails to repay the loan, the lender can repossess or foreclose on the collateral. However, unlike recourse loans, the lender cannot sue the borrower for additional repayment.

Because lenders take on more risk with non‑recourse financing, these loans often come with:

- Higher interest rates

- Stricter underwriting standards

- Larger down payment requirements

- More detailed asset evaluations

Despite these hurdles, the liability protection they offer can be worth the trade‑off.

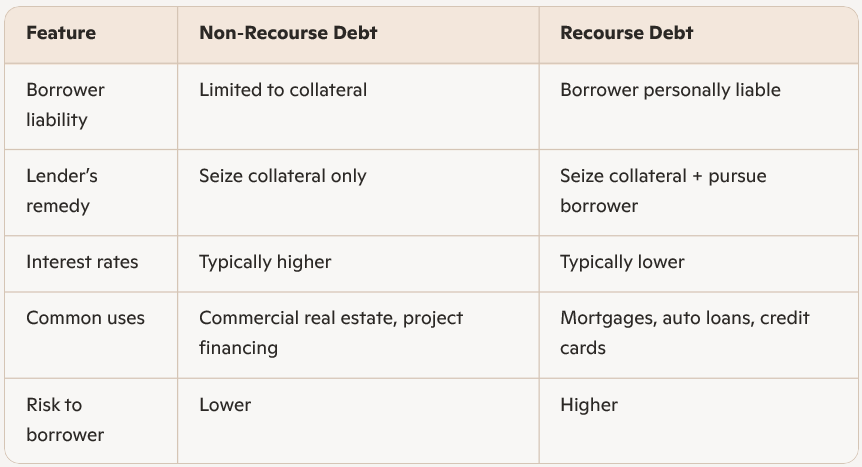

Non‑Recourse vs. Recourse Debt

Understanding the difference between recourse and non‑recourse debt is essential for evaluating risk.

For investors, the key advantage of non‑recourse debt is asset protection. Even if a project fails, personal wealth remains shielded.

Where Non‑Recourse Debt Is Most Common

While non‑recourse loans exist in several industries, they are most prevalent in:

1. Commercial Real Estate

Non‑recourse financing is widely used for:

- Multifamily properties

- Office buildings

- Retail centers

- Industrial facilities

Lenders rely heavily on the property’s income stream and market value rather than the borrower’s personal guarantee.

2. Project and Infrastructure Financing

Large‑scale projects—such as energy developments, toll roads, and public‑private partnerships—often use non‑recourse structures to isolate risk.

3. Self‑Directed Retirement Accounts

Investors using a Self‑Directed IRA (SDIRA) to buy real estate must use non‑recourse loans due to IRS rules. This protects the retirement account from prohibited transactions and personal liability.

4. Asset‑Backed Business Loans

Some equipment financing and business loans are structured as non‑recourse when the collateral is highly valuable and easily recoverable.

Advantages of Non‑Recourse Debt

Non‑recourse financing offers several strategic benefits:

1. Personal Asset Protection

The borrower’s liability is limited to the collateral. Personal savings, income, and other assets remain protected.

2. Risk Mitigation for Investors

If a project underperforms or market conditions shift, the borrower can walk away without facing deficiency judgments.

3. Attractive for Long‑Term Wealth Building

Investors can leverage assets without exposing their entire financial portfolio to risk.

4. Compliance Benefits for Retirement Accounts

For SDIRA investors, non‑recourse loans are often the only compliant way to finance real estate purchases.

Disadvantages of Non‑Recourse Debt

While beneficial, non‑recourse loans come with trade‑offs:

1. Higher Interest Rates

Lenders charge more to offset the increased risk.

2. Stricter Qualification Requirements

Borrowers may need:

- Strong credit

- High‑value collateral

- Larger down payments

- Proven investment experience

3. “Bad Boy” Carve‑Outs

Many non‑recourse loans include clauses that convert the loan to recourse if the borrower commits fraud, waste, or intentional misconduct.

4. Limited Availability

Not all lenders offer non‑recourse financing, especially for smaller residential properties.

Is Non‑Recourse Debt Right for You?

Non‑recourse debt can be a smart choice if you:

- Want to protect personal assets

- Are investing in commercial or income‑producing real estate

- Need financing for a Self‑Directed IRA

- Prefer to limit downside exposure

- Are comfortable with higher interest rates and stricter terms

However, if you’re seeking lower rates, easier qualification, or financing for a primary residence, recourse loans may be more practical.

Final Thoughts

Non‑recourse debt is a valuable tool for investors and businesses looking to limit personal liability while leveraging high‑value assets. By understanding how these loans work—and the trade‑offs involved—you can make more informed decisions that align with your financial goals and risk tolerance.

If you’re exploring real estate investing, project financing, or SDIRA strategies, non‑recourse debt may offer the protection and flexibility you need to build long‑term wealth.