Section 1202 of the Internal Revenue Code often referred to as the Qualified Small Business Stock (QSBS) exclusion is one of the most powerful tax incentives available to founders, early employees, and startup investors. When structured correctly, Section 1202 allows eligible taxpayers to exclude up to 100% of capital gains on the sale of qualified stock, potentially eliminating millions of dollars in federal tax liability. With recent legislative updates increasing exclusion caps and expanding eligibility, Section 1202 gains have become even more valuable for high‑growth companies planning future exits.

This guide breaks down how Section 1202 works, who qualifies, how much gain can be excluded, and the key rules every business owner and investor must understand.

What Are Section 1202 Gains?

Section 1202 gains are capital gains realized from the sale of Qualified Small Business Stock that meet the requirements of IRC §1202. For eligible non‑corporate taxpayers, these gains may be partially or fully excluded from federal income tax if the stock is held for the required period and the issuing corporation meets strict criteria.

Under current law, Section 1202 allows for 50%, 75%, or 100% exclusion, depending on when the stock was acquired and how long it was held. For many founders and investors, this can turn a large taxable exit into a nearly tax‑free one.

What Counts as Qualified Small Business Stock (QSBS)?

To generate Section 1202 gains, the stock must meet all QSBS requirements at issuance and throughout the holding period. Key criteria include:

1. The Issuer Must Be a Domestic C Corporation

Only C‑corporations can issue QSBS. LLCs, partnerships, and S‑corps do not qualify. If a business starts as an LLC, it must convert to a C‑corp before exceeding the asset threshold to preserve QSBS eligibility.

2. The Company Must Be a Qualified Small Business

At the time of issuance and immediately after, the corporation’s aggregate gross assets must not exceed $75 million (increased from $50 million under recent legislation). This limit applies to post‑2025 stock and is indexed for inflation beginning in 2027.

3. The Stock Must Be Acquired at Original Issuance

You must receive the shares directly from the company in exchange for:

- Cash

- Property (other than stock)

- Services (e.g., founder or employee equity)

Purchases from other shareholders do not qualify.

4. The Company Must Conduct an Active Qualified Trade or Business

At least 80% of the company’s assets must be used in an active business. Certain industries are excluded, including:

- Health, law, engineering, architecture

- Accounting and financial services

- Hospitality, hotels, and restaurants

- Banking, insurance, and leasing

The rules favor innovative, product‑driven, and technology‑focused businesses.

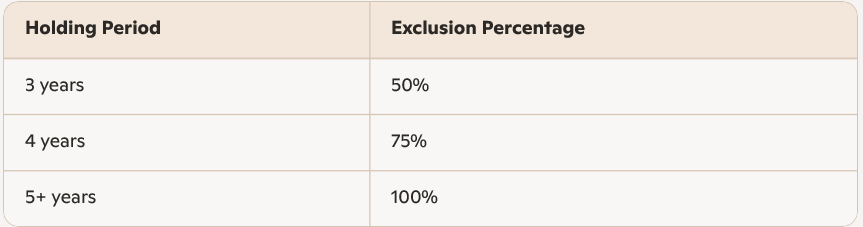

Section 1202 Exclusion Percentages and Holding Periods

The amount of gain you can exclude depends on when the stock was acquired and how long you held it.

For QSBS acquired after July 4, 2025:

This tiered system rewards longer holding periods while offering earlier partial exclusions.

For QSBS acquired before the new applicable date:

Most post‑2010 QSBS still qualifies for a 100% exclusion after five years, preserving the highly favorable pre‑2026 rules.

Exclusion Limits: How Much Gain Can Be Tax‑Free?

Section 1202 includes a per‑issuer cap on the amount of gain you can exclude.

For QSBS acquired after July 4, 2025:

- Greater of $15 million (indexed for inflation starting 2027), or

- 10× your basis in the stock

For QSBS acquired before that date:

- Greater of $10 million, or

- 10× basis

This means a founder who converts an LLC to a C‑corp at a $2 million valuation could potentially exclude up to $20 million in future gains an enormous tax advantage.

Why Section 1202 Matters for Founders and Investors

Section 1202 is one of the few provisions in the tax code that can eliminate federal capital gains tax entirely. For startups and high‑growth companies, this creates several strategic benefits:

1. More Attractive to Investors

Angel investors and venture capitalists often factor QSBS eligibility into their investment decisions. A potential 100% tax‑free exit significantly boosts after‑tax returns.

2. Encourages Early‑Stage Innovation

The rules are designed to support small, innovative businesses by rewarding long‑term investment and growth.

3. Major Tax Savings at Exit

For founders, early employees, and seed investors, Section 1202 can reduce federal tax liability by millions of dollars sometimes more than the company’s early‑stage funding rounds.

Maintaining QSBS Eligibility

QSBS status can be lost if the company:

- Fails the 80% active business test

- Exceeds the asset threshold before issuance

- Engages in disqualifying redemptions

- Converts out of C‑corp status

Founders should work closely with tax advisors to ensure compliance throughout the holding period.

Conclusion

Section 1202 gains represent one of the most powerful tax incentives available to entrepreneurs and investors. With the potential to exclude up to 100% of capital gains, QSBS treatment can dramatically increase after‑tax exit proceeds. As 2026 rules expand exclusion caps and introduce tiered holding periods, understanding and planning for Section 1202 has never been more important.

Whether you’re forming a startup, raising capital, or planning a future exit, structuring your business to qualify for QSBS can unlock extraordinary tax benefits and potentially transform your long‑term financial outcome.

This article provides information only and should not be construed as advice. It is provided without warranty of any kind.