What Is Debt to Income Ratio?

The debt-to-income (DTI) ratio compares your monthly debt obligations to your gross monthly income. Expressed as a percentage, it helps lenders evaluate how much of your income is already committed to debt and whether you can afford additional credit.

Formula:

Debt To Income Ratio = Total Monthly Debt Payments\Gross Monthly Income times 100

For example, if your monthly debts total $1,500 and your gross income is $5,000, your DTI ratio is:

(1500 ÷ 5000) \times 100 = 30\%

This means 30% of your income goes toward debt payments.

Why DTI Ratio Matters

Lenders use DTI to gauge your financial stability and risk level. A high DTI suggests you may struggle to take on new debt, while a low DTI indicates better financial flexibility.

Key reasons DTI matters:

- Loan approvals: Mortgage lenders often require a DTI below 43%, though 36% is preferred.

- Interest rates: Lower DTI can qualify you for better rates.

- Financial health: High DTI may signal over-extension and risk of default.

What’s Included in DTI Calculations?

When calculating DTI, include all recurring monthly debt payments:

- Mortgage or rent

- Credit card minimum payments

- Auto loans

- Student loans

- Personal loans

- Alimony or child support

Exclude non-debt expenses like utilities, groceries, and insurance premiums.

Types of DTI Ratios

There are two main types of DTI:

1. Front-End DTI

This measures housing-related expenses (mortgage, property taxes, insurance) against income. It’s crucial for mortgage applications.

2. Back-End DTI

This includes all monthly debt payments. Most lenders focus on this when assessing overall financial health.

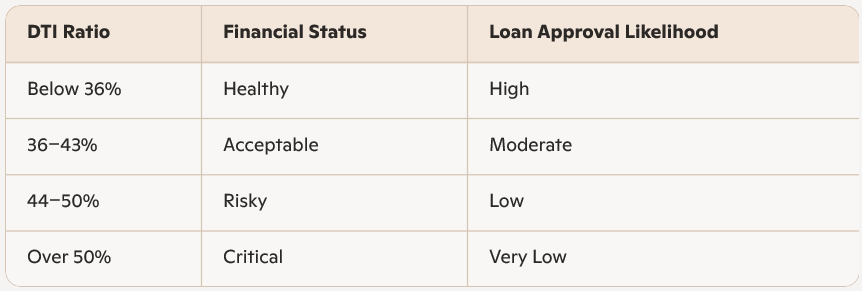

What Is a Good DTI Ratio?

While ideal DTI thresholds vary by lender and loan type, here’s a general guide:

How to Improve Your Debt To Income Ratio

If your DTI is too high, here are actionable steps to reduce it:

- Pay down debt: Focus on high-interest loans first.

- Increase income: Take on freelance work, a side hustle, or negotiate a raise.

- Avoid new debt: Delay large purchases or new credit applications.

- Refinance loans: Lower monthly payments through better terms.

- Review credit reports: Ensure accuracy to avoid inflated debt figures.

Debt To Income Ratio vs Credit Score

While your DTI ratio doesn’t directly affect your credit score, the factors that influence DTI—like credit card balances—can impact your score. Maintaining low balances and timely payments benefits both metrics.

Debt To Income Ratio in Mortgage Applications

Mortgage lenders scrutinize DTI closely. The Consumer Financial Protection Bureau recommends a maximum DTI of 43% for qualified mortgages. Some lenders may allow higher ratios with compensating factors like strong credit or large down payments.

Business Applications of A Debt To Income Ratio

DTI isn’t just for individuals. Small businesses also use DTI to assess financial health and creditworthiness. Investors may examine a company’s debt-to-income metrics to evaluate risk and sustainability.

Final Thoughts

Your debt-to-income ratio is more than just a number—it’s a snapshot of your financial health. Whether you’re applying for a mortgage, managing personal debt, or planning for future financial goals, understanding and optimizing your DTI can unlock better opportunities and long-term stability.